SkyeChip – mini-Broadcom in the making

18 May 2026

Leveraging cutting edge technology in becoming ASIC silicon supplier.

We are glad to witness this landmark moment for Malaysia. The upcoming listing of SkyeChip represents the culmination of decades of learning, hard work, experience, and entrepreneurial vision by a talented team of engineers, led by an ambitious founding team with strong business acumen and relentless drive. SkyeChip is set to become the first truly cutting-edge semiconductor IP company to be listed on Bursa Malaysia.

SkyeChip, led by its talented engineering team and co-founding CTO Teh Chee Hak, began its journey as an intellectual property (IP) owner — no easy feat in the semiconductor industry. Please refer to our previous article for further insights into the development of an IC design business. SkyeChip has demonstrated strong capabilities in developing cutting-edge semiconductor IP that is silicon-proven, meaning its designs have been successfully fabricated into actual chips.

Engineering ingenuity is essential in this industry. Over the past 17 years, we have encountered many engineering-driven companies that ultimately struggled to scale, often due to the absence of ambitious leadership with strong commercial instincts. Building an IP business from the ground up — especially as an IP vendor without proven silicon in its early stages — demands far more than technical capability. It requires a leader with ambition, resilience, business acumen, strategic foresight, and deep industry relationships. In this respect, founding CEO Dato’ Fong Swee Kiang is exceptionally well-suited for leading the company.

Currently, it is supported by 365 engineers. The company holds 36 registered patents and 77 pending applications across Malaysia, China, and the USA — a meaningful IP moat for a company of its size.

This article is an attempt to crystallize my thought and shed some light on the framework to think about the visibility of such business. I would try to keep this piece as simple as possible to read while leaving slightly more technical details in the appendix.

Business Model (IP and ASIC)

Semiconductor IP refers to pre-designed, pre-verified reusable circuit blocks that IC designers integrate into their chips (SoCs, FPGAs, ASICs) instead of building these building blocks from scratch.

SkyeChip specializes in the design and licensing of silicon IP cores — primarily memory interface IP (LPDDR4/5/6, HBM3/3E/4) and Network-on-Chip (NoC) IP, Die-to-Die (D2D) interface IP — as well as the development of custom ASICs for third-party clients and JV in the ownerships of silicon products.

Currently, SkyeChip licenses IP on a project-by-project lump-sum basis. In the future, it is also possible to Introduce per-chip royalty components to generate a recurring royalty revenue.

SkyeChip’s Semiconductor IP business model is predicated on two structural rationales:

Reusability — a single IP core design can be licensed to many customers across different projects, generating recurring revenue at minimal marginal cost. In this regard, this is like software companies, once software created, you can sell many copies; and

Time-to-market — chip designers save 6-18 months of development effort by licensing rather than designing complex blocks internally. As process nodes shrink below 7nm and complexity rises, the economic rationale for IP licensing only strengthens.

SkyeChip’s custom ASIC (Application Specific IC) business model comprises two broad revenue streams:

Custom ASIC design services – SkyeChip doesn’t focus on pure design services unless the customers also acquired its IP in the development of the ASIC. Hence, it would generate both design service revenue and IP revenue at the same time.

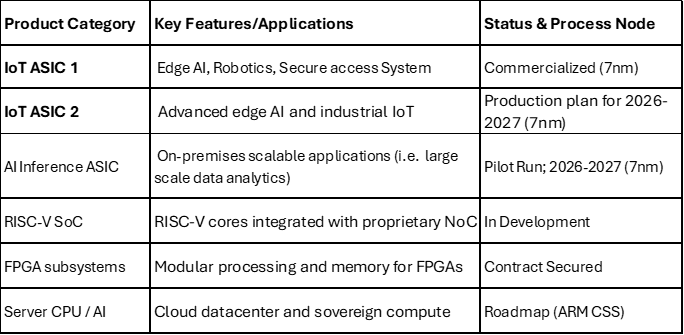

Silicon product business – SkyeChip has secured two contracts with Customer D to jointly develop IoT ASICs incorporating its proprietary IP. The first product, an Edge AI computing chip, has already been commercialized.

The company derives revenue from non-recurring engineering (NRE) fees, IP licensing fees, as well as chip sales on a cost-plus basis in selected geographical regions outside its partner’s designated markets.

Visibility and Growth Prospects

Investors who are new to this sector might feel the business of IP licensing appears to be one-off and visibility seems limited; the fact is that the business could also be resilient and keep growing in a fast-expanding market if one has the right technology and team.

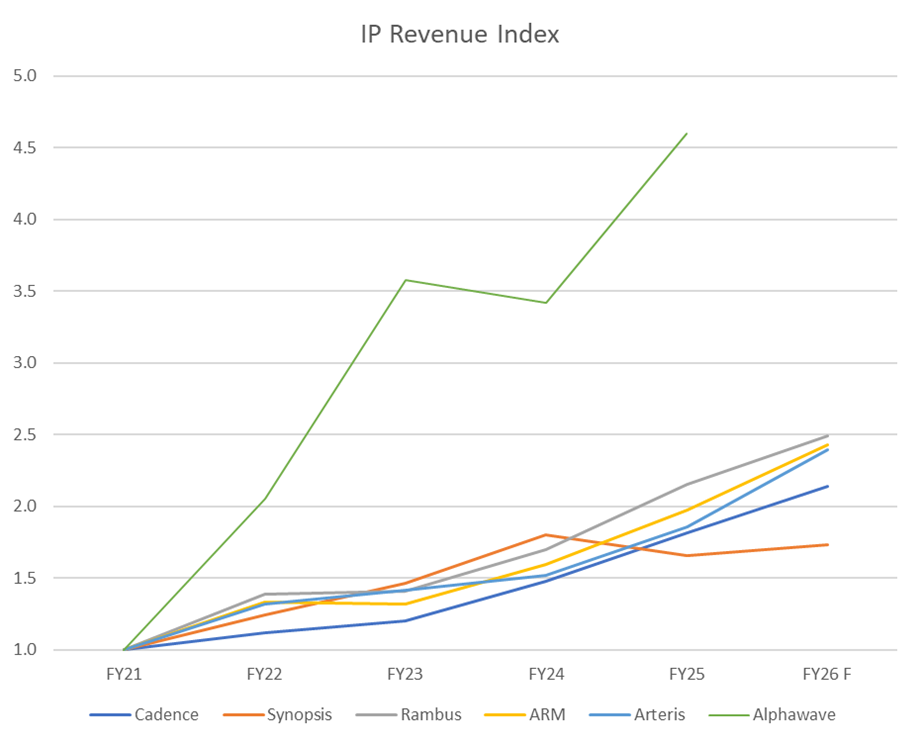

source: Bloomberg

source: Bloomberg

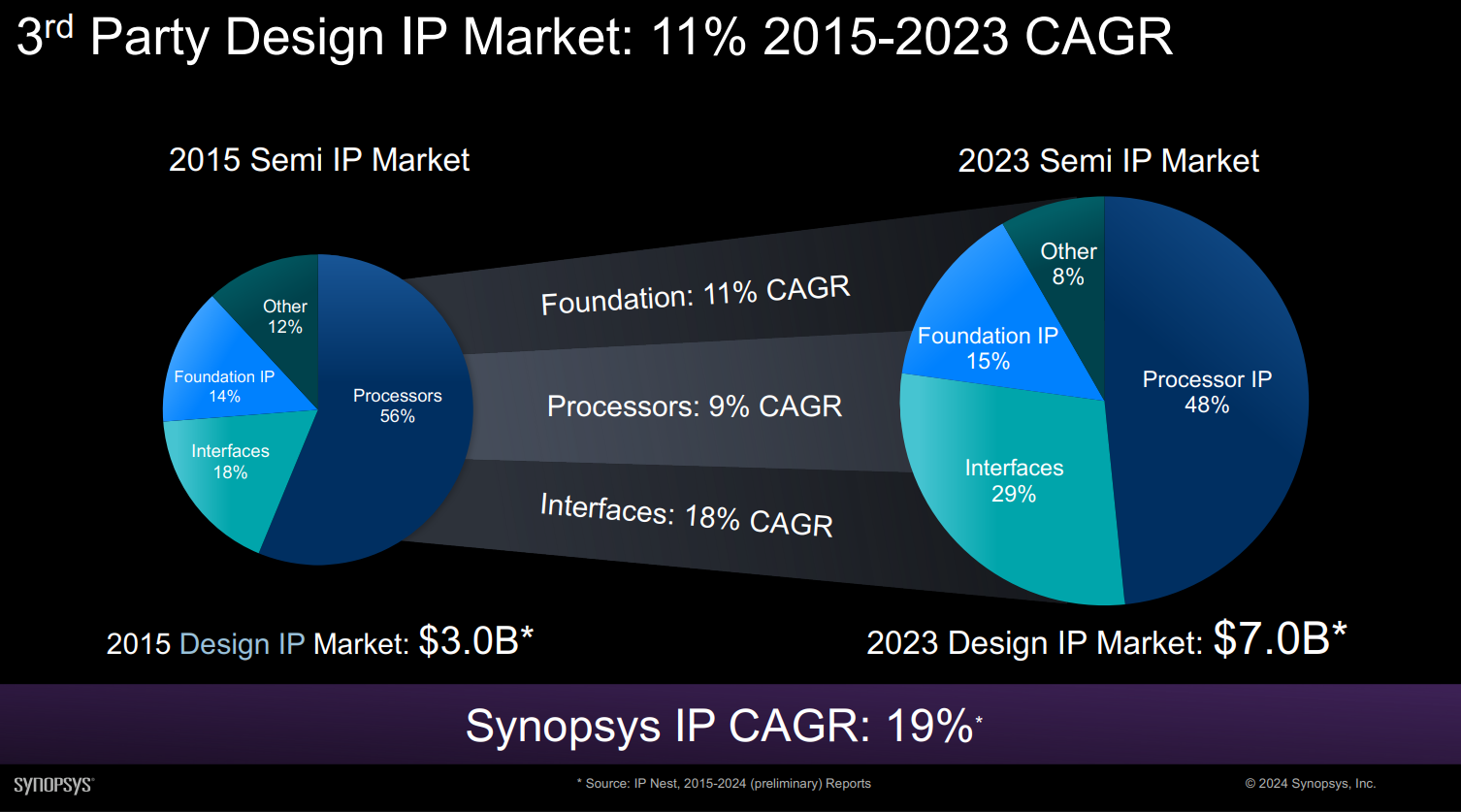

This chart shows the IP-related revenue of SkyeChip’s competitors (p.s. ARM isn’t a competitor), the compounded annual growth rate (CAGR) of these sizable companies is around 15% to 20% per annum. (Alphawave has been acquired by Qualcomm.) As a comparison, SkyeChip’s revenue CAGR has been around 30% since 2022.

The visibility and growth of IP business can be viewed from 3 angles, which are (1) Total Addressable Market expansion, (2) Moats and (3) Expanding the source of revenue.

Total Addressable Market (TAM) expansion

The TAM itself has been growing rapidly thanks to several factors:

Time-to-Market

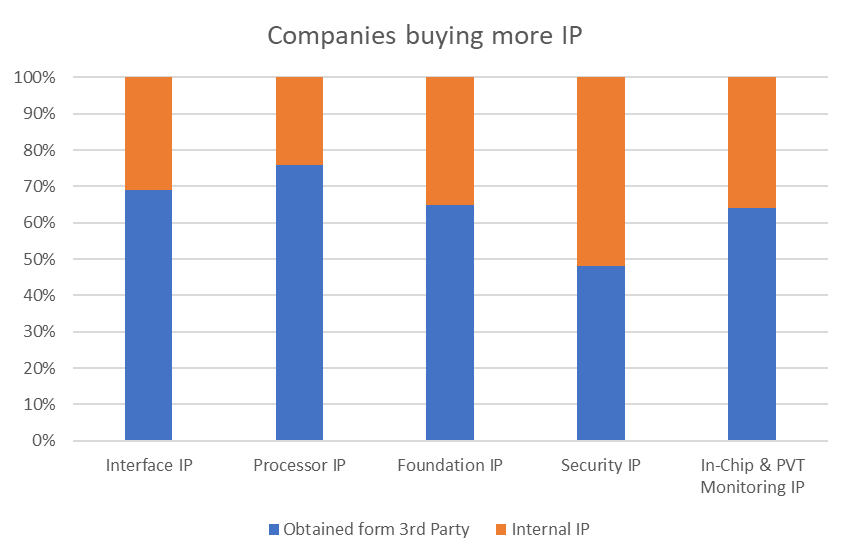

Chip companies increasingly buy IP because as complexity rises, it is better to buy proven wheel than to reinvent it. Buying IP accelerates development by 6-18 months. The AI chip product cycle operates at a significantly faster pace — roughly 1–2 years — compared to the traditional 3–5-year cycle of central processing units (CPUs), driven by the need to keep pace with explosive token demand. source: Synopsis presentation slide

source: Synopsis presentation slide The relentless pursuit of efficiency

The explosive demand in AI led to a bottleneck in electricity and water resources. Customers are always chasing for better efficiency. As Jensen Huang said argued that extreme co-design—the simultaneous optimization of hardware, software, and algorithms—is the fundamental driver of efficiency in modern computing. AI Chip company needs to continuously enhance its architecture and move its design forward to a more advanced process node to stay competitive, these creates a sustained demand for IP.AI Chip startup surge

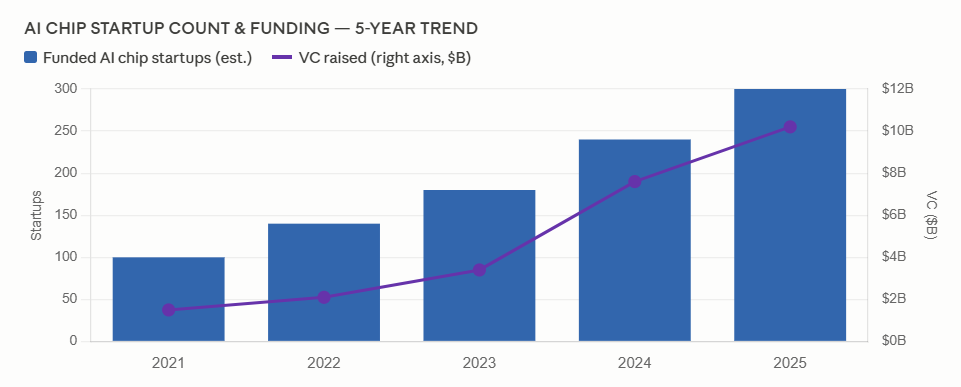

source: 2025 VC Report

source: 2025 VC Report

AI chip startups have grown from ~100 funded companies in 2021 to 300+ in 2025, with funding accelerating sharply from USD4 bn in 2021 to USD12bn in 2025. The strategy of these startups is to focus on its core competencies and buy the available IP design to integrate and develop its product.System-on-Chip (SoC) growth driving Network-On-Chip demand

NoC IP outsourcing is an emerging field rising on the back rapid introduction of SoCs. SoC helps to optimize power, performance and area efficiency of chip, make it ever more powerful yet smaller.Bandwidth Wall driving HBM standard advancement

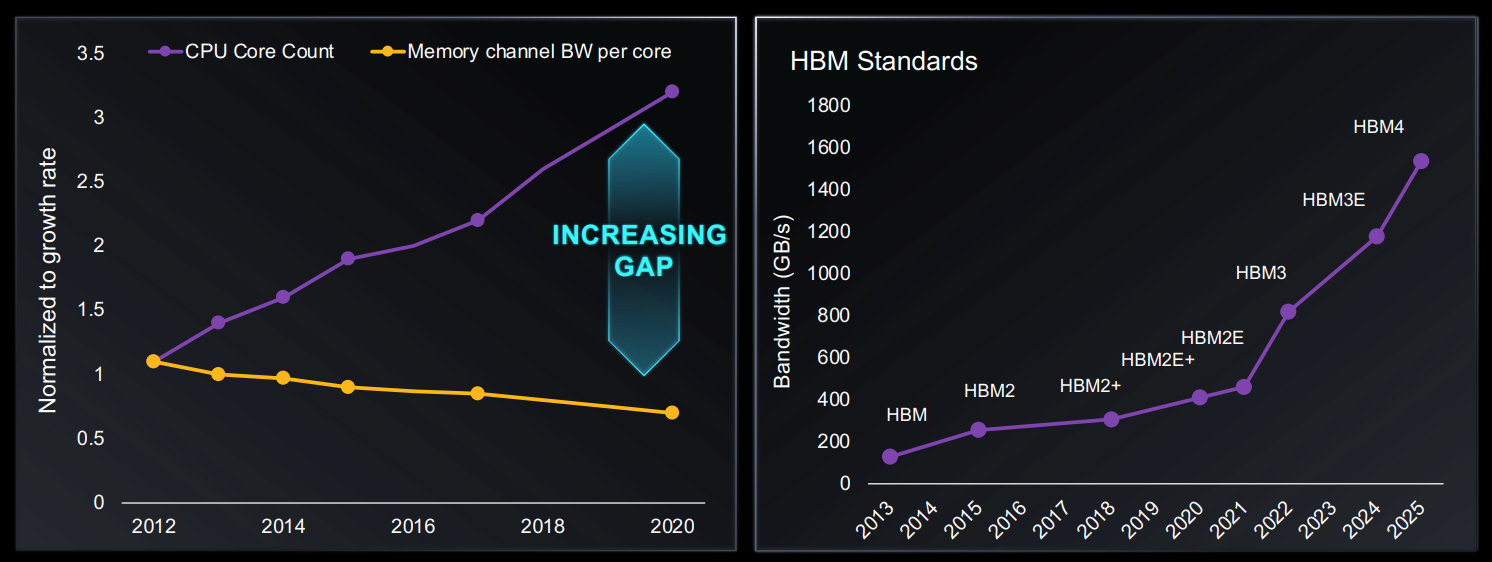

source: Meta OCP & Synopsis presentation

source: Meta OCP & Synopsis presentation

In modern computing, the speed which processor (CPU, GPU, or AI accelerator) can compute data far exceeds the speed at which it can receive that data from memory. This chart shows the rising gap of memory bandwidth per core propelling the HBM Standards forward. SkyeChip started with HBM3 in 2022 and is now developing HBM4.Higher Average Selling Price (ASP)

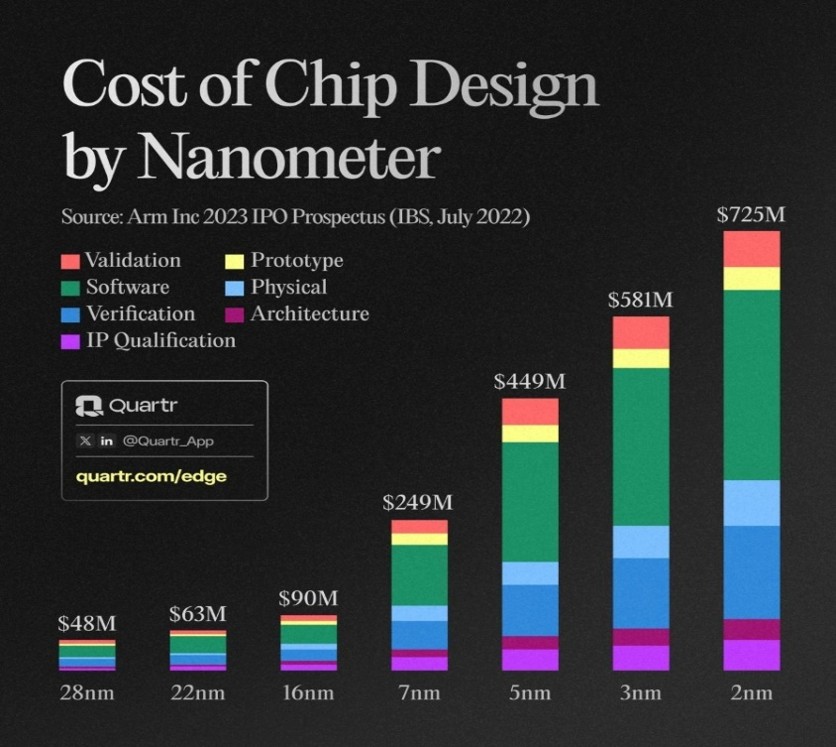

source: Quartr

source: Quartr

As IP design moves towards a more advanced node, the ASP goes up. Moving from 16nm to 3nm increased design costs by roughly 7x, emphasizing that 3nm requires a total redesign of IP and verification, with software accounting for a huge portion of the budget.Based on various industry sources, the current HBM3/3E/4 IP pricing is around USD3.5m to USD5m with US companies selling at a meaningful premium. NoC and LPDDR5/5x IP starts from USD0.5m to USD2m. We expect the ASP to continue moving upwards as complexity increased.

Chiplets/Multi die trend driving D2D IP demand

As Moore’s Law Slows, chiplets have emerged as the primary, dominant response to the physical and economic limits of scaling, helping to overcome the limitations of building ever-larger silicon dies which has lower yield.The rise of Chiplets led to a surge in advanced packaging, which is known as CoWos in TSMC and EMIB & Foveros in Intel. If you have listened to TSMC result briefing in the recent years, you must have heard of CoWos given that it is the real bottleneck of getting more chips out.

Proliferation of chiplets lead to (i) more design starts, (ii) more interfaces, especially UCIe D2D, (iii) more IP in multiple foundries and (iv) more IP In multiple nodes.

Channel Expansion

SkyeChip has been working on expanding its accessible market. It started with mainly China centric customers in the founding years then added Taiwanese customers and now US companies have begun to adopt it IP. It plans to set up sales and R&D office in the US to further expand into the market.

source: Prospectus; Quarterly Result

source: Prospectus; Quarterly Result

Moats / Competitive advantages

Having a large and growing market is one thing, more importantly is understanding of why customers would choose and stick with you.

Silicon-Proven

It means the IP has been physically manufactured, measured on real silicon, and passed validation. This matters because a failed chip tape-out can cost millions of dollars and set a programme back by 6 to 12 months. Customers cannot afford to be anyone's guinea pig, which is why incumbents like SkyeChip enjoy a moat.Access to foundries advanced nodes and leading OSAT

SkyeChip holds access to advanced nodes (7nm and below) across all three leading foundries — TSMC, Samsung, and Intel Foundry. This is increasingly rare. Both TSMC and Samsung have reportedly halted shipments of sub-7nm chips to Chinese IC firms, effectively locking out a large portion of potential competitors from the most critical manufacturing tier.China counts over 3,500 IC design houses, but the number capable of taping out advanced chips at scale — with the engineering depth, customer base, EDA, packaging ecosystem, and foundry relationships to match — is fewer than five.

Foundry access is also inseparable from PDK access. To design a chip compatible with a given manufacturing process, a team must have the foundry's process design kit in hand. Without it, there is no viable path to production.

source: Oaklands Path

source: Oaklands Path The majority of SkyeChip's competitors are US-headquartered and it increasingly cuts them off from the fast-growing Chinese market. While most Chinese chip firms are not sanctioned, there is a clear preference to source from non-American vendors where alternatives exist. Innosilicon would otherwise be a formidable rival, but its loss of access to advanced nodes has significantly weakened its position. SkyeChip's Malaysian domicile carries a quiet strategic advantage here — as a neutral country, it carries none of the geopolitical baggage that shadows American peers, making it a naturally palatable partner for customers on both sides of the divide.

We should also note that SkyeChip is in the whitelist of world leading OSAT (likely to be ASE) with advanced packaging capability.

Flexibility with Multiple Foundries access

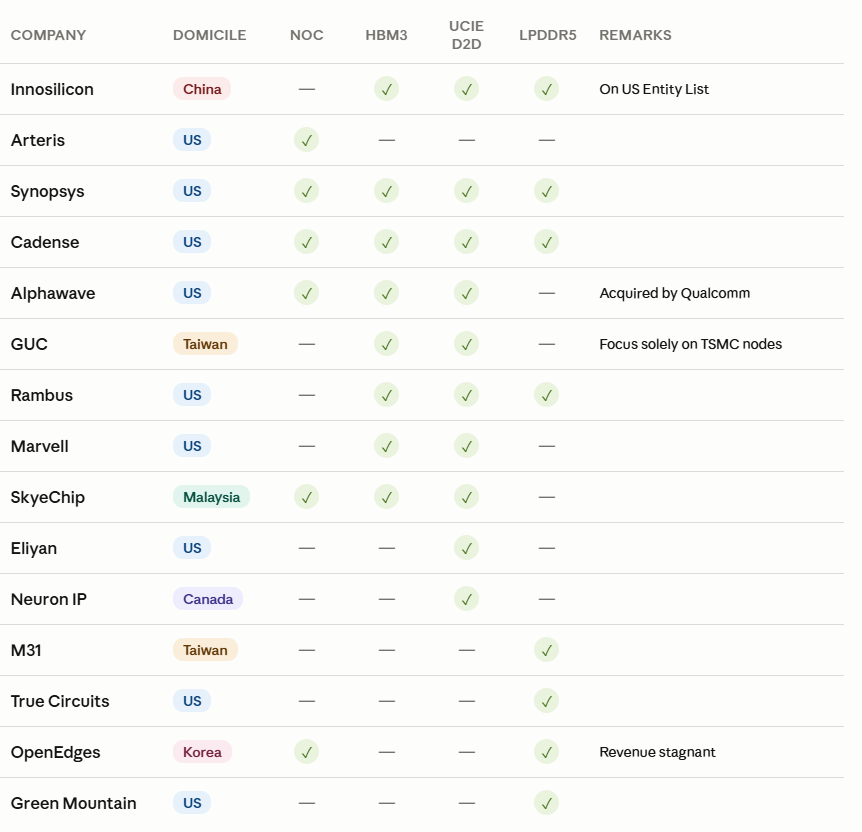

In the high-stakes world of AI chip manufacturing, access to "factory space" (foundry capacity) is the ultimate bottleneck. Currently, TSMC’s cutting-edge 3nm capacity is effectively monopolized by giants like NVIDIA and Apple. For a chip designer, creating a "digital blueprint" (IP) is useless if there are no available fabs to build it.SkyeChip solves this problem through Foundry Portability. Unlike many competitors, SkyeChip has optimized its flagship HBM3/3E IP to work across both TSMC (12nm and 7nm) and Samsung (4nm) platforms. This flexibility allows SkyeChip to win high-value contracts that its rivals cannot fulfil. For example, dominant players like GUC and Alchip are strategically locked into a "TSMC-only" model. GUC is even 35% owned by TSMC. By maintaining an open and neutral relationship with all three leading foundries (TSMC, Samsung, and Intel), SkyeChip provides its customers with a vital "Plan B," ensuring their AI products can reach the market even when the world's primary factories are full.

Quality of the IP

SkyeChip competes directly against global incumbents to secure cutting-edge IP licensing deals across China, Taiwan, and the United States. While investors often find it difficult to assess technical performance, SkyeChip’s credibility is anchored in a definitive industry gold standard: "First-Pass Silicon Success". A landmark example is their HBM3E interface IP, which was successfully validated on a leading-edge 4nm process node at speeds of 8,800 Mbps on the very first fabrication runIn the semiconductor world, failure is catastrophically expensive; a single design error in a complex AI chip can cost millions of dollars and set a product roadmap back by 6 to 12 months. By delivering "silicon-proven" designs, meaning their digital blueprints have already been physically manufactured and tested in real-world conditions, SkyeChip eliminates these massive financial and timing risks for their clients. This verified track record, combined with a growing base of returning customers and a formidable moat of 113 filed patents, proves that SkyeChip possesses the technical mastery required to lead the global AI infrastructure market.

Breadth of relevant IP portfolio

Customers naturally gravitate toward fewer vendors — fewer integration points means fewer risks and less coordination overhead. An AI-focused vendor like SkyeChip, offering NoC, high-speed memory interfaces, and UCIe D2D chiplet connectivity under one roof, becomes strategically attractive precisely because it reduces that complexity.Staying Ahead through access to standard setting associations

SkyeChip holds membership in JEDEC and UCIe — the standards-setting organisations behind technologies such as HBM, DDR, LPDDR, and UCIe D2D. Active participation grants early visibility into where specifications are heading, allowing SkyeChip to begin designing next-generation IP in compliance with international standards before those standards are publicly finalised.Roadmap Alignment

Customers — particularly AI ASIC firms, which operate on unusually fast product upgrade cycles — want to work with vendors who have a credible and committed roadmap for future nodes. This is the same logic behind Jensen Huang's habit of publicly announcing chips that are two or three generations out.Reputation

Beyond engineering, semiconductor industry purchasing is relationship-driven. A CTO will rarely risk: a multi-hundred-million-dollar chip on an unknown vendor without references.Faster customization and better service

Smaller vendors can often move faster — customising to customer requirements, iterating on designs, and providing direct access to senior engineers rather than routing requests through layers of account management. Large Western incumbents, for all their resources, can be slow and bureaucratic.Resource and Performance Tuner (RAPTuner) with NoC IP

SkyeChip's NoC is the first in the world that is able to reconfigure routing paths after tapeout. It is a scalable and area-efficient interconnect solution optimized for memory systems.Complementing this is RAPTuner (Resource and Performance Tuner), SkyeChip's proprietary simulation and optimisation tool built in lockstep with our NoC IP. RAPTuner streamlines the full interconnect configuration process, from traffic profiling and topology selection to post-silicon routing adjustments, replacing months of manual analysis with a simulation-driven flow. Because RAPTuner is co-designed with the NoC hardware, its routing outputs map directly to the reconfiguration registers embedded in silicon, a closed loop no third-party tool can replicate. For fabless customers who would otherwise spend years on a bespoke in-house interconnect, this is a decisive shortcut to a validated, production-ready solution.

Expanding the source of revenue

SkyeChip began as a semiconductor IP vendor but has since leveraged its high-speed interface portfolio to move further up the value chain — co-developing two custom IoT ASICs in 2023. The ultimate goal is to become customer silicon partner of customer in co-designing and selling proprietary AI inference ASICs, backed by secured manufacturing capacity at leading-edge foundries and sold at volume. In essence, SkyeChip is following the same trajectory Broadcom took, using deep IP expertise as the foundation for a full custom silicon business.

Let’s digress a bit and looked at the development of Broadcom.

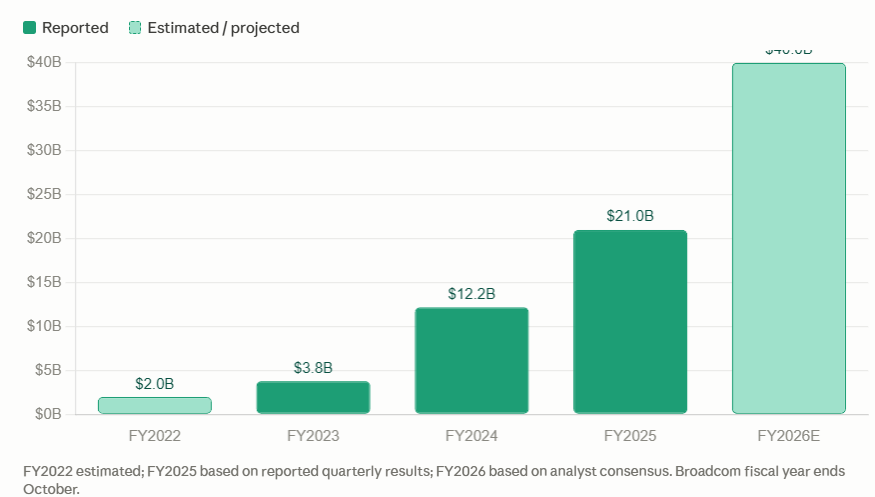

Broadcom’s custom AI ASIC revenue

Under the leadership of Hock Tan, Broadcom took a very different approach from companies like Nvidia and AMD. Instead of selling standardized chips to everyone, Broadcom became the “custom silicon partner” for hyperscaler like Google, Meta, Bytedance and recently OpenAI.

Mr Tan led Broadcom and acquired LSI Corporation and Avago to build up its cutting-edge high-speed SerDes interconnect IP, which are essential for connecting thousands of AI cores/TPUs together for large-scale AI training. It then leverages it into winning custom AI ASIC for customers. The Google TPU is perhaps the most prominent example of what this looks like in practice: Broadcom oversees the full ASIC design, ensures manufacturability, and manages chip fabrication and packaging through third-party foundries — principally TSMC — before delivering finished silicon to Google at gross margins north of 65%.

Now let’s go back to SkyeChip’s. It is well-positioned to serve Asian hyperscalers, AI labs, and fabless chip companies that lack internal silicon design teams. Its expanding revenue source includes:

Custom ASICs and silicon products

SkyeChip has won 6 contracts for the design and development of custom silicon products as reported. It is also eyeing to win business in the AI hardware accelerator for Data preprocessing as well as Security ASIC.

High-performance CPU and AI platforms – aiming to be made by Malaysia

In May 2026, SkyeChip received approval to access an Arm Flexible Access (AFA) token under the Malaysia-Arm Silicon Vision partnership — a licence that typically costs millions of dollars and is rarely granted to firms outside of the largest global chip companies. Meanwhile, it is still waiting for final approval for the access to ARM Compute Subsystem (CSS) token.Developing cutting-edge silicon from the ground up is enormously capital-intensive, and building advanced CPU or AI chips demands far more than IC design expertise alone. Access to Arm's leading-edge compute cores is vital but only part of the equation — system architecture knowledge and software depth are equally critical and rarely reside within a single organisation.

SkyeChip's strategy is to combine its high-speed interface and NoC IP with the AFA/CSS access to bring in a credible technology partner with the system and software expertise needed to jointly develop a high-performance CPU targeted at AI applications.

If successful, this transforms SkyeChip from an IP licensor into a silicon product company capable of selling CPUs/AI platforms — a fundamentally higher-value business with potentially much larger revenue scale.

Automotive IP (ISO 26262 compliant NoC) – structural growth

The global automotive semiconductor market is projected to double to USD100B+ by 2030. ADAS systems and autonomous driving require complex SoCs with advanced memory and NoC interfaces. Automotive-grade IP commands a premium over consumer-grade IP and creates multi-year, sticky customer relationships. SkyeChip targets commercialization of ISO 26262-compliant NoC IP in 2026-2027.2.5D/3D chiplet products - Capitalising on Advanced Packaging

The semiconductor industry's migration to chiplet architectures (exemplified by AMD's 3D V-Cache, Intel's EMIB/Foveros, TSMC's SoIC/CoWoS) creates demand for Die-to-Die (D2D), Memory I/O chiplets and CIM (Compute-in-Memory) silicon dies. SkyeChip's planned CIM dies and I/O chiplets target this next wave of packaging innovation.

Risk areas

While we are optimistic on SkyeChip's prospects, the following risks merit attention:

Geopolitical and Customer Concentration - China and Taiwan combined account for approximately 70% of revenue, leaving the business meaningfully exposed to cross-strait tensions and US-China trade policy.

Tax Incentive Expiry – SkyeChip has applied for an extension of its Malaysian tax incentive, though approval is not guaranteed. The company has also secured incentives in Vietnam, which provides some offset.

Talent & R&D Execution – Rapid technology obsolescence demands continuous R&D spend. An IP business is ultimately only as strong as its engineering team. We have high conviction in the technical team led by Chee Hak, but retention and execution remain areas to monitor.

Regulatory & Export Control Risk – Like all IP firms, SkyeChip's design workflow depends on EDA tools from Synopsys, Cadence, and Ansys. US BIS export control rules on semiconductor design tools and IP are evolving, and any tightening could introduce operational disruption.

Product diversification execution — SkyeChip's expansion beyond its core IP business into custom silicon and high-performance CPU platforms is still at an early stage and execution risk remains.

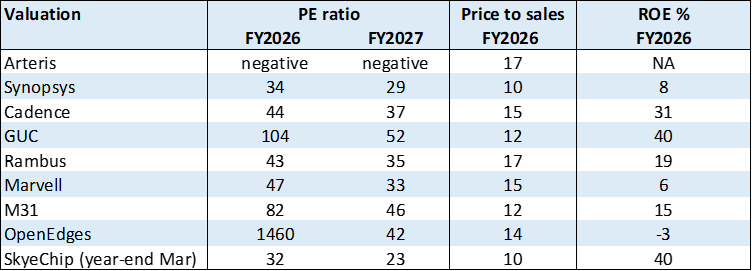

Valuation

source: Bloomberg

source: Bloomberg

Conclusion

SkyeChip has carefully built up its critical high-speed IP portfolios, like Broadcom in the early stage. SkyeChip’s memory interface IP expertise is directly synergistic with AI accelerator design — Every AI accelerator, whether implemented as a monolithic SoC or a chiplet-based architecture, requires NoC fabric for internal performance optimisation and HBM or LPDDR controllers for external memory bandwidth. SkyeChip's IP sits squarely in that critical path.

Combined with its access advanced nodes in all three foundries as well as leading advanced packaging OSAT, and being in a neutral country, made it uniquely well positioned to serve Asian fabless chip companies, hyperscaler as well as the new wave of US AI chip startups.

With expanding channel, IP reuse and relicensing economics improve, cross-selling opportunities across adjacent IP categories multiply, and the custom ASIC design services business gains both scale and reference customers.

The pending approver for ARM CSS access, if materializes, gives is a strategic advantage to move forward in design customer high-performance CPU chip for AI use. This is a large market that did not exist on SkyeChip's roadmap until recently.

The current AI Supercycle has created extraordinary and sustained demand for custom silicon design globally. We are optimistic that SkyeChip under the leadership of Dato Fong and Chee Hak would ride this trend well in the years ahead.

Appendix

Interface IP is the second biggest market in IP outsourcing and is the fastest growing

source: Synopsis presentationThe interface IP sub-segment — SkyeChip's market — is growing materially faster than total design IP, driven by: (i) rising SoC complexity (more interfaces per die), (ii) chiplet / heterogeneous integration (D2D/UCIe explicitly needed), (iii) HBM-bound AI accelerators, and (iv) the shift to advanced nodes where in-house interface design becomes uneconomic for all but hyperscalers.

The market has grown from USD 3.0bn (2015) to roughly USD 7.0bn in 2023, and IPnest forecasts it reaching approximately USD 4.75bn for Interface IP alone by 2028, with the full market tracking toward ~USD 14–15bn.

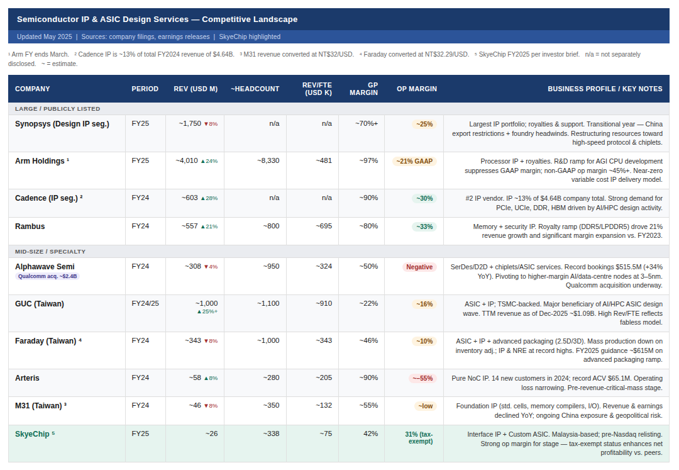

Peer Comparison — Headcount and Margin Benchmarks

SkyeChip revenue per headcount is relatively lower now, which is consistent with (a) lower average US-benchmarked price per IP deal, (b) a still-immature sales / re-use engine, and (c) Malaysian engineer cost base that is roughly 40% of US levels. However, its operating margin is a respectable 30% range.

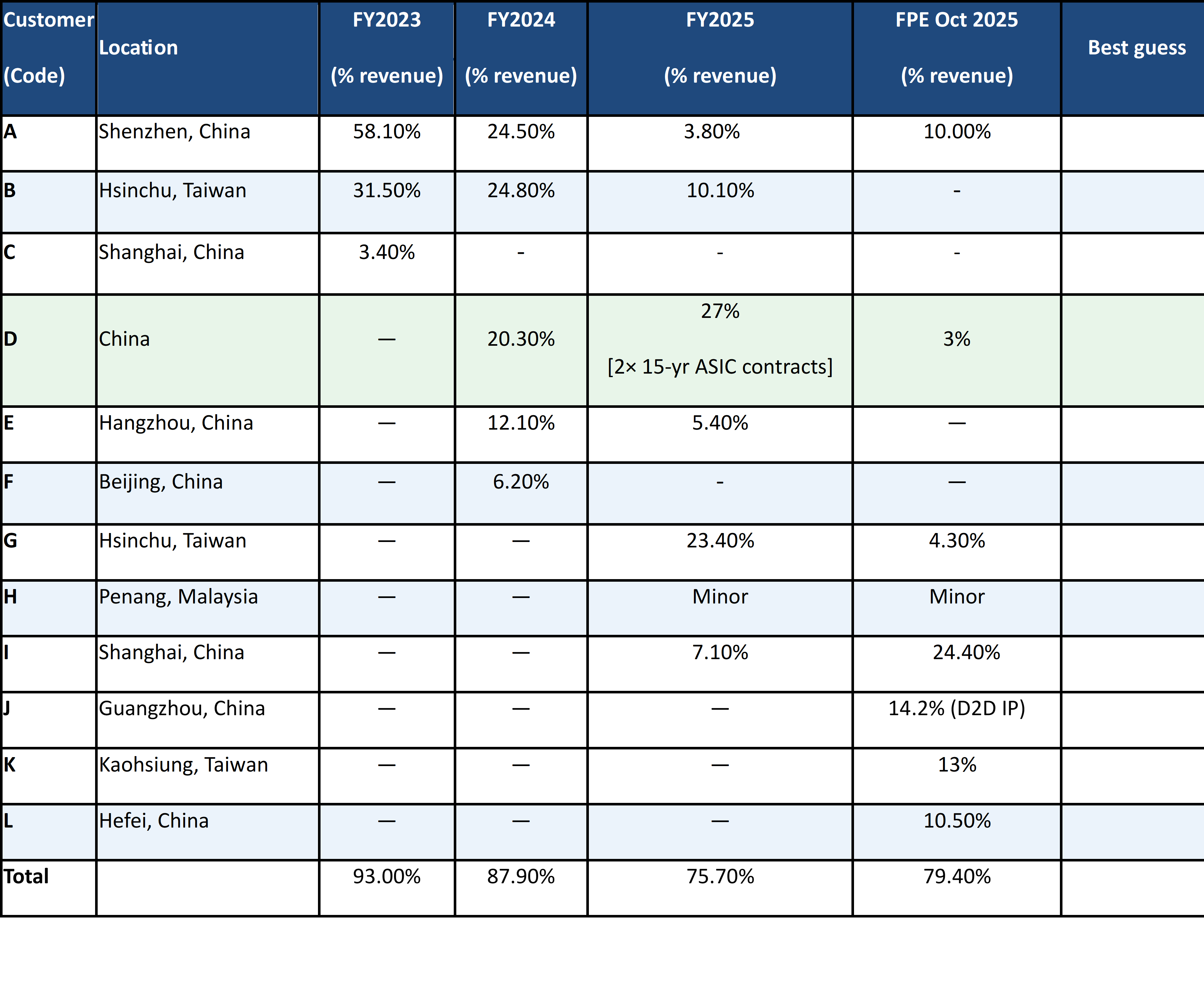

Customer Analysis SkyeChip does not disclose its some of its supplier and most of its customers, the below is based on our best guess from information available on the web and prospectus, we cannot provide assurance that it is accurate.

source: prospectus

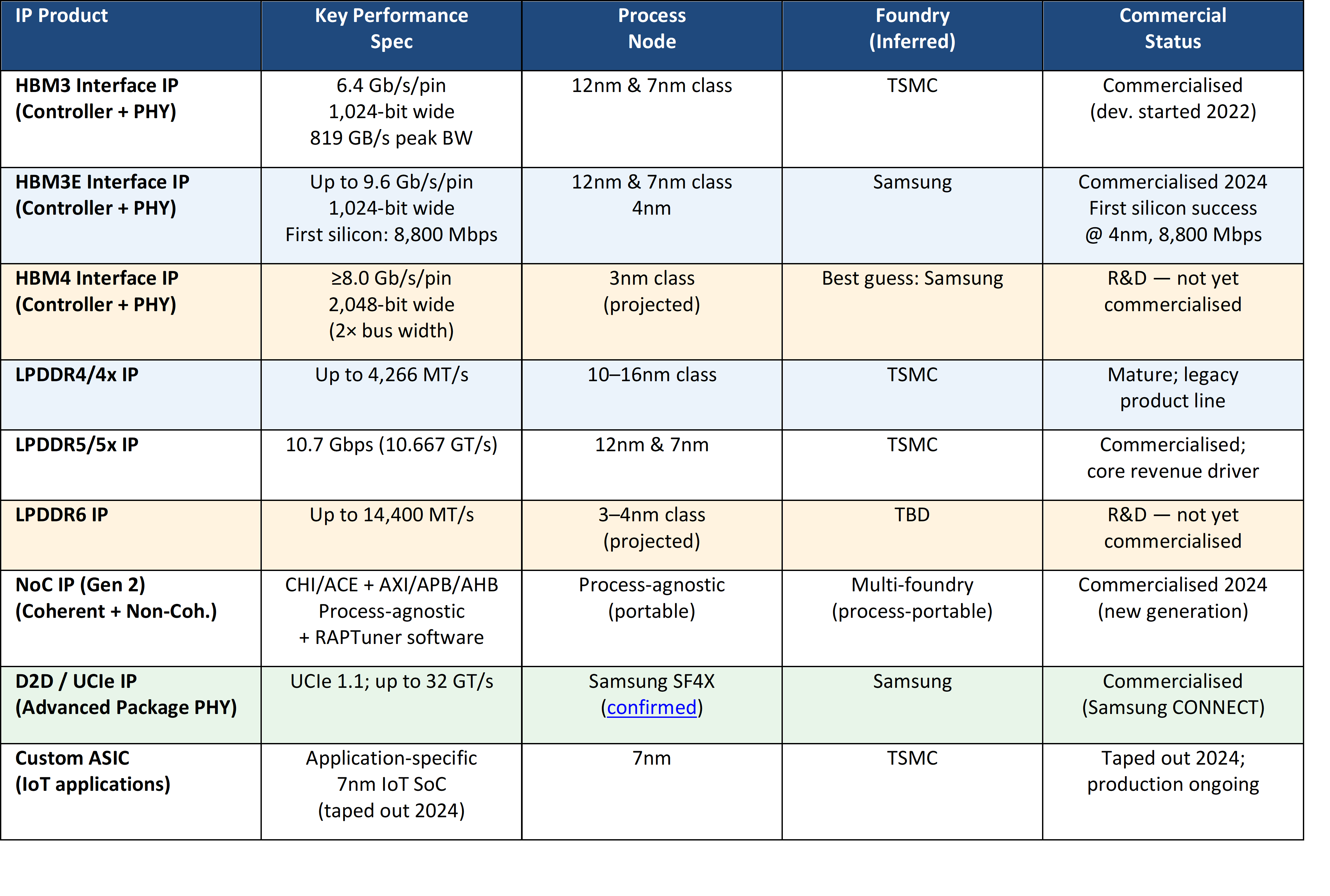

source: prospectus IP Product Technical Specifications by Process Node

SkyeChip does not disclose its some of its supplier and most of its customers, the above is based on our best guess from information available on the web and prospectus, we cannot provide assurance that it is accurate. Note: Amber rows = IP products currently in R&D (not yet generating revenue). Green row = D2D/UCIe IP on Samsung Foundry SF4X (LN04LPP), listed on Samsung Foundry CONNECT — the only foundry affiliation confirmed by name in public disclosures.

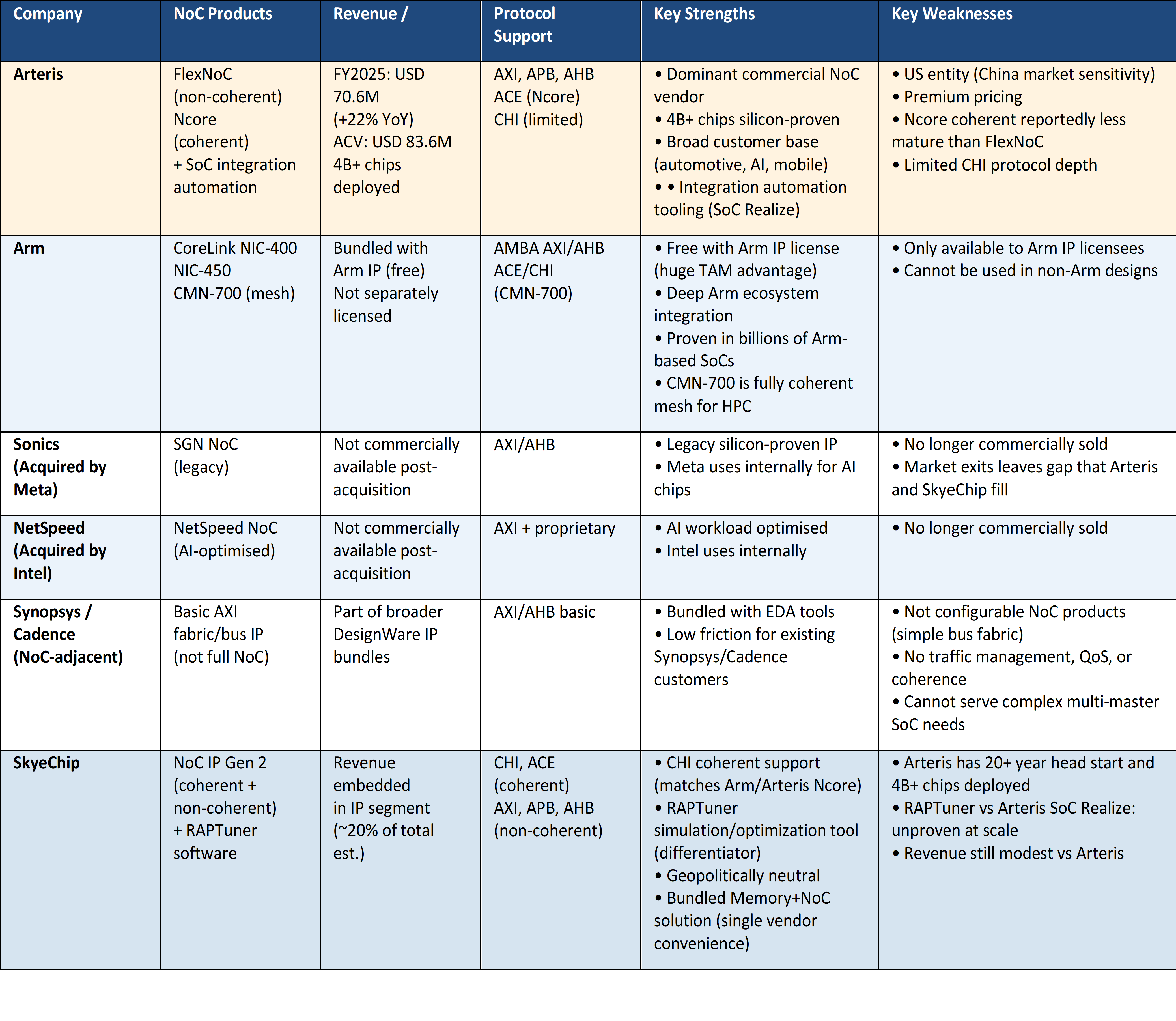

Note: Amber rows = IP products currently in R&D (not yet generating revenue). Green row = D2D/UCIe IP on Samsung Foundry SF4X (LN04LPP), listed on Samsung Foundry CONNECT — the only foundry affiliation confirmed by name in public disclosures.Network-on-Chip (NoC) IP: Competitive Landscape

source: various websites.

source: various websites.

The NoC market is structurally compelling opportunity for SkyeChip. Arteris is the only significant commercial competitor remaining after Meta acquired Sonics and Intel acquired NetSpeed.

Notes and Disclaimers

This essay and the information contained herein is not a specific offer of products or services. Information on this essay is not an offer to buy or sell, or a solicitation of any offer to buy or sell the securities mentioned herein.

Oaklands Path may be long or short the securities mentioned herein and has no duty or obligation to disclose or update our action on these securities.

This essay contains information and views as of the date indicated and such information and views are subject to change without notice. We have no duty or obligation to update the information contained herein. Further, we make no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Although we obtain information contained in our newsletter from sources we believe to be reliable, we cannot guarantee its accuracy. Moreover, independent third-party sources cited in these materials are not making any representations or warranties regarding any information attributed to them and shall have no liability in connection with the use of such information in these materials.